June CPI Report and Fed Chair Warsh Testimony Set to Move Markets

Tuesday's inflation data and Fed Chair Kevin Warsh's Capitol Hill testimony headline a week that could reset rate expectations.

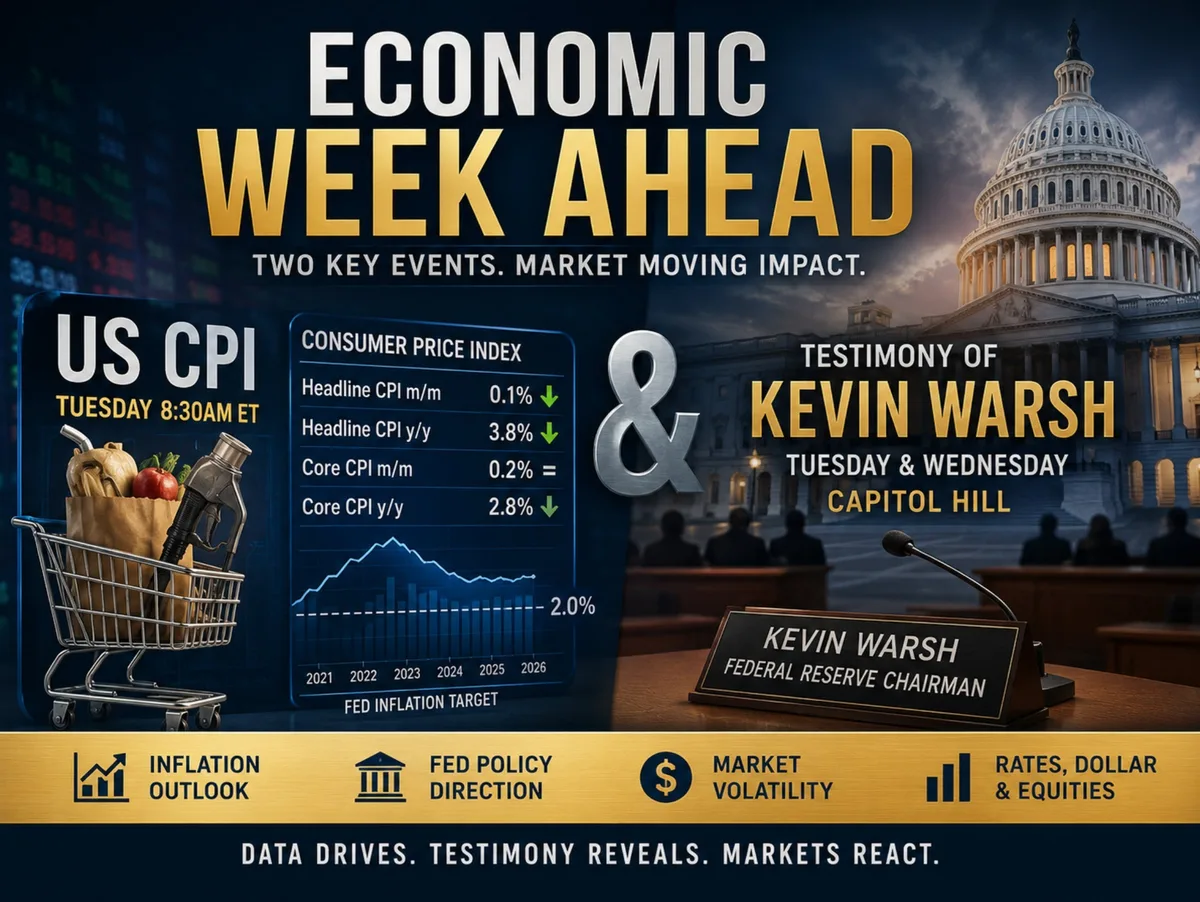

Two high-stakes events this week — Tuesday's June CPI release and Federal Reserve Chairman Kevin Warsh's semiannual congressional testimony — have the power to reprice expectations for U.S. monetary policy and trigger broad swings across equities, the dollar, Treasury yields, and precious metals. The CPI report drops at 8:30 AM ET Tuesday; Warsh faces the House Financial Services Committee just 90 minutes later at 10:00 AM ET, then returns for a Senate Banking Committee appearance Wednesday.

Economists forecast headline CPI rose just 0.1% month-over-month in June, down sharply from May's 0.5% reading and the softest monthly print since June 2025. Year-over-year, headline inflation is projected to slow to 3.8% from 4.2%, while core CPI — which strips out food and energy — is expected to tick down to 2.8% annually from 2.9%. Both readings remain well above the Fed's 2% target. For context, headline CPI has not fallen below 2% since March 2021, illustrating just how entrenched inflation has become.

Read more New Zealand Services Sector Returns to Growth With June PSI at 50.6 →

The implications of Tuesday's data are asymmetric. A cooler-than-expected print would reinforce a Fed-on-hold narrative, pressuring the dollar and boosting risk assets. A surprise to the upside, however, could revive chatter about additional rate hikes, sending Treasury yields and the dollar higher while punishing equities and bonds — a scenario that felt remote just months ago but the Fed has refused to fully rule out.

Warsh's testimony arrives with a pre-released Fed Report to Congress already on the table. That document described an economy slowing at the household level but buoyed by AI-driven investment, improving productivity, and a resilient labor market. The Fed's updated projections trimmed its 2026 growth outlook only modestly to 2.2%, while raising headline and core CPI forecasts sharply to 3.6% and 3.3%, respectively. The projected unemployment rate was simultaneously lowered to 4.3%, signaling policymakers see no meaningful labor market deterioration on the horizon.

Beyond the prepared remarks, traders will be watching the unscripted Q&A sessions closely. Warsh has been actively distancing the Fed from the era of forward guidance — signaling at the ECB Forum in Sintra that the central bank intends to communicate less about future rate paths and more through its actual decisions. With fresh inflation data in hand, any shift in tone could prove to be the most market-moving moment of the week. Continue reading at Forexlive.